Fair Price Estimation#

The utility indifference theory for derivatives pricing#

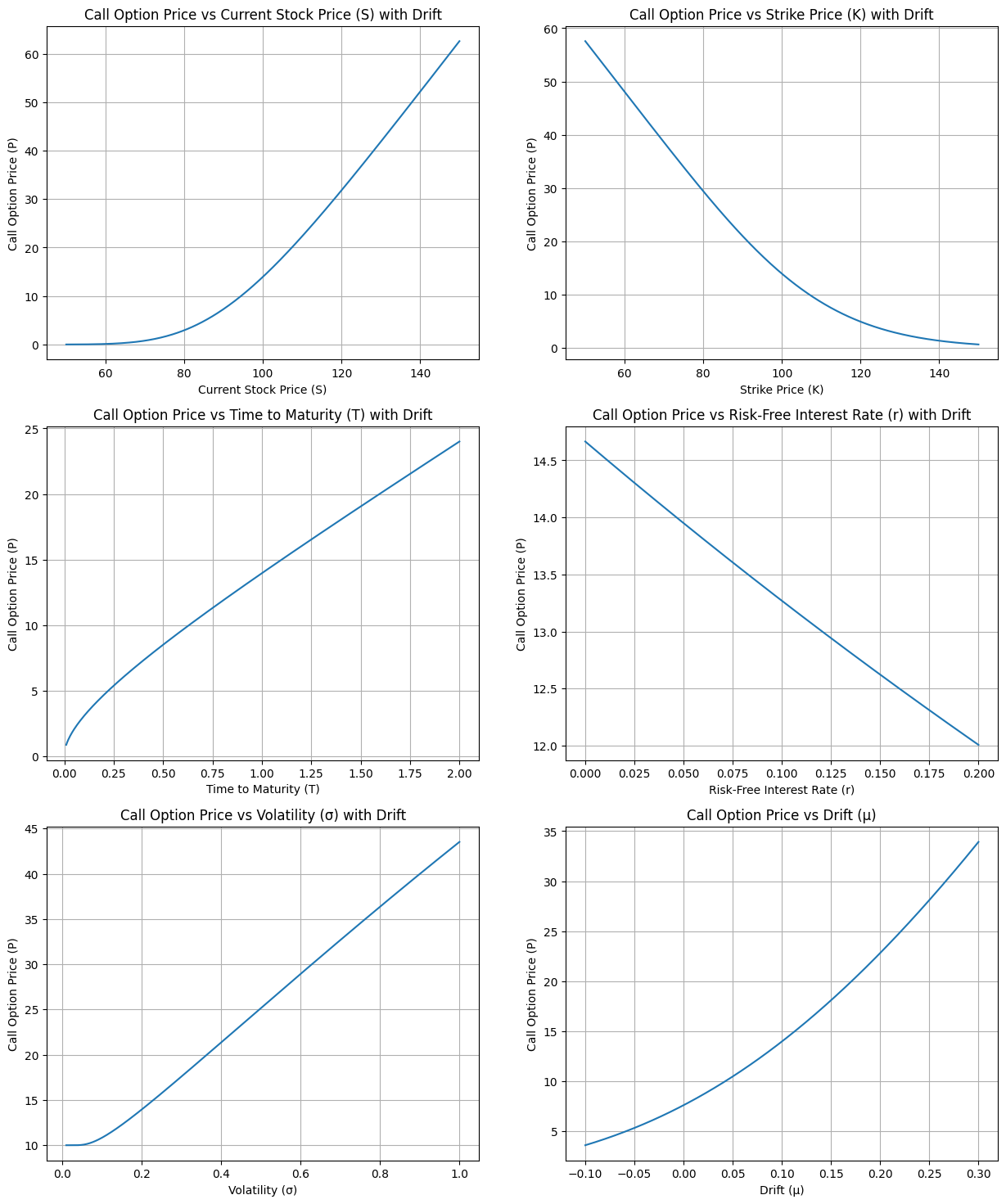

Call option premium using the utility indifference principle#

import numpy as np

import matplotlib.pyplot as plt

from scipy.stats import norm

# Black-Scholes formula with drift implementation

def black_scholes_with_drift(S, K, T, t, r, mu, sigma):

d1_mu = (np.log(S / K) + (mu + 0.5 * sigma**2) * (T - t)) / (sigma * np.sqrt(T - t))

d2_mu = d1_mu - sigma * np.sqrt(T - t)

call_price_with_drift = S * np.exp((mu - r) * (T - t)) * norm.cdf(d1_mu) - K * np.exp(-r * (T - t)) * norm.cdf(d2_mu)

return call_price_with_drift

# Parameters for the plots

S_t = 100 # Current stock price

K = 100 # Strike price

T = 1 # Time to maturity (1 year)

t = 0 # Current time (now)

r = 0.05 # Risk-free interest rate (5%)

mu = 0.1 # Drift rate (10%)

sigma = 0.2 # Volatility (20%)

# Generate data for each dependency plot

S_values = np.linspace(50, 150, 400)

K_values = np.linspace(50, 150, 400)

T_values = np.linspace(0.01, 2, 400)

r_values = np.linspace(0, 0.2, 400)

sigma_values = np.linspace(0.01, 1, 400)

mu_values = np.linspace(-0.1, 0.3, 400)

# Calculate call prices with drift

C_S_drift = [black_scholes_with_drift(S, K, T, t, r, mu, sigma) for S in S_values]

C_K_drift = [black_scholes_with_drift(S_t, K, T, t, r, mu, sigma) for K in K_values]

C_T_drift = [black_scholes_with_drift(S_t, K, T, t, r, mu, sigma) for T in T_values]

C_r_drift = [black_scholes_with_drift(S_t, K, T, t, r, mu, sigma) for r in r_values]

C_sigma_drift = [black_scholes_with_drift(S_t, K, T, t, r, mu, sigma) for sigma in sigma_values]

C_mu_drift = [black_scholes_with_drift(S_t, K, T, t, r, mu, sigma) for mu in mu_values]

# Plotting all dependencies in a single figure for export

fig, axs = plt.subplots(3, 2, figsize=(15, 18))

# Current Stock Price (S) with Drift

axs[0, 0].plot(S_values, C_S_drift)

axs[0, 0].set_title('Call Option Price vs Current Stock Price (S) with Drift')

axs[0, 0].set_xlabel('Current Stock Price (S)')

axs[0, 0].set_ylabel('Call Option Price (P)')

axs[0, 0].grid(True)

# Strike Price (K) with Drift

axs[0, 1].plot(K_values, C_K_drift)

axs[0, 1].set_title('Call Option Price vs Strike Price (K) with Drift')

axs[0, 1].set_xlabel('Strike Price (K)')

axs[0, 1].set_ylabel('Call Option Price (P)')

axs[0, 1].grid(True)

# Time to Maturity (T) with Drift

axs[1, 0].plot(T_values, C_T_drift)

axs[1, 0].set_title('Call Option Price vs Time to Maturity (T) with Drift')

axs[1, 0].set_xlabel('Time to Maturity (T)')

axs[1, 0].set_ylabel('Call Option Price (P)')

axs[1, 0].grid(True)

# Risk-Free Interest Rate (r) with Drift

axs[1, 1].plot(r_values, C_r_drift)

axs[1, 1].set_title('Call Option Price vs Risk-Free Interest Rate (r) with Drift')

axs[1, 1].set_xlabel('Risk-Free Interest Rate (r)')

axs[1, 1].set_ylabel('Call Option Price (P)')

axs[1, 1].grid(True)

# Volatility (σ) with Drift

axs[2, 0].plot(sigma_values, C_sigma_drift)

axs[2, 0].set_title('Call Option Price vs Volatility (σ) with Drift')

axs[2, 0].set_xlabel('Volatility (σ)')

axs[2, 0].set_ylabel('Call Option Price (P)')

axs[2, 0].grid(True)

# Drift (μ)

axs[2, 1].plot(mu_values, C_mu_drift)

axs[2, 1].set_title('Call Option Price vs Drift (μ)')

axs[2, 1].set_xlabel('Drift (μ)')

axs[2, 1].set_ylabel('Call Option Price (P)')

axs[2, 1].grid(True)

The arbitrage-free theory of derivatives pricing#

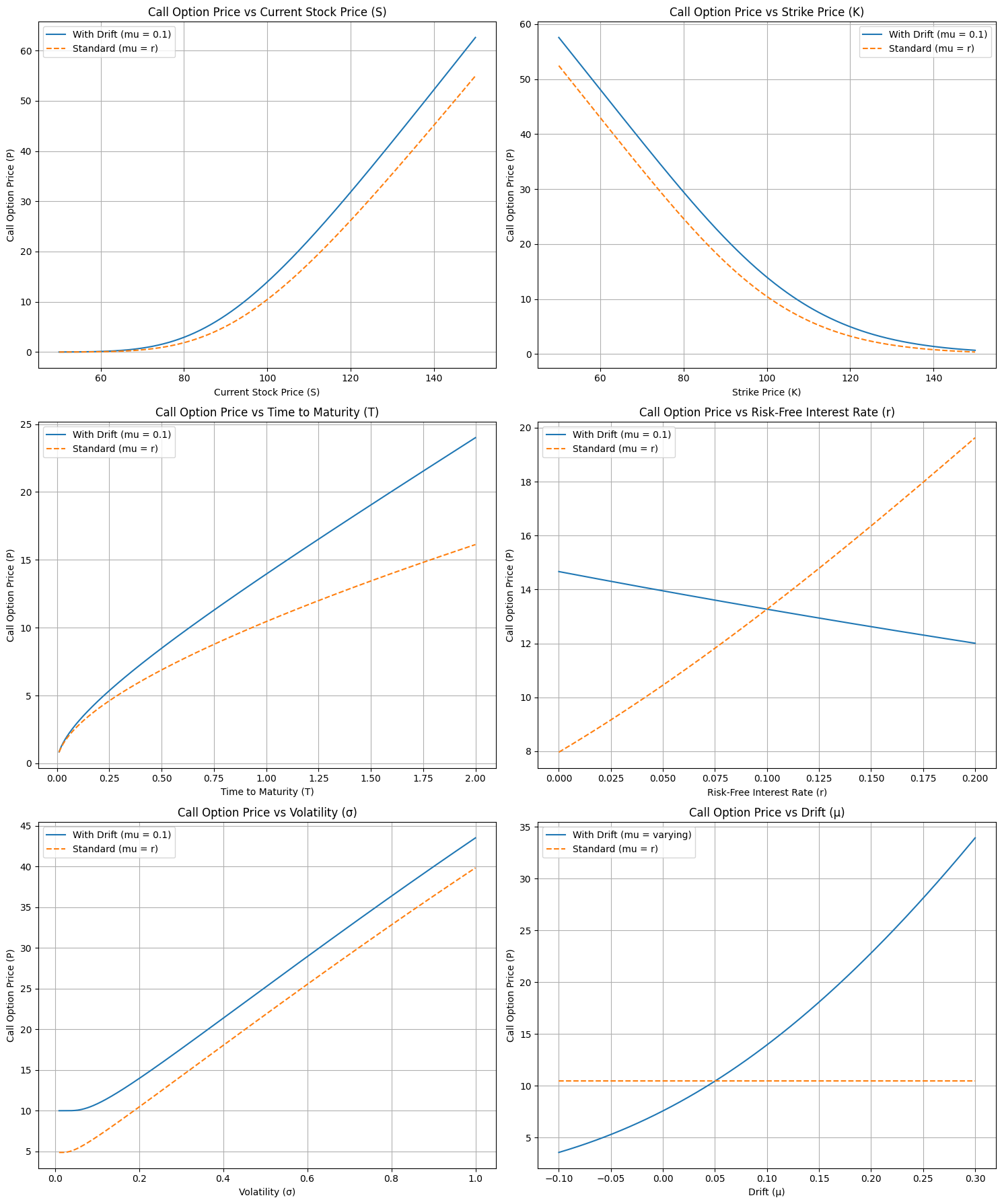

Call option premium using arbitrage-free theory#

import numpy as np

import matplotlib.pyplot as plt

from scipy.stats import norm

# Black-Scholes formula with drift implementation

def black_scholes_with_drift(S, K, T, t, r, mu, sigma):

d1_mu = (np.log(S / K) + (mu + 0.5 * sigma**2) * (T - t)) / (sigma * np.sqrt(T - t))

d2_mu = d1_mu - sigma * np.sqrt(T - t)

call_price_with_drift = S * np.exp((mu - r) * (T - t)) * norm.cdf(d1_mu) - K * np.exp(-r * (T - t)) * norm.cdf(d2_mu)

return call_price_with_drift

# Standard Black-Scholes formula (mu = r)

def black_scholes_standard(S, K, T, t, r, sigma):

return black_scholes_with_drift(S, K, T, t, r, r, sigma)

# Parameters for the plots

S_t = 100 # Current stock price

K = 100 # Strike price

T = 1 # Time to maturity (1 year)

t = 0 # Current time (now)

r = 0.05 # Risk-free interest rate (5%)

mu = 0.1 # Drift rate (10%)

sigma = 0.2 # Volatility (20%)

# Generate data for each dependency plot

S_values = np.linspace(50, 150, 400)

K_values = np.linspace(50, 150, 400)

T_values = np.linspace(0.01, 2, 400)

r_values = np.linspace(0, 0.2, 400)

sigma_values = np.linspace(0.01, 1, 400)

mu_values = np.linspace(-0.1, 0.3, 400)

# Calculate call prices with drift

C_S_drift = [black_scholes_with_drift(S, K, T, t, r, mu, sigma) for S in S_values]

C_K_drift = [black_scholes_with_drift(S_t, K, T, t, r, mu, sigma) for K in K_values]

C_T_drift = [black_scholes_with_drift(S_t, K, T, t, r, mu, sigma) for T in T_values]

C_r_drift = [black_scholes_with_drift(S_t, K, T, t, r, mu, sigma) for r in r_values]

C_sigma_drift = [black_scholes_with_drift(S_t, K, T, t, r, mu, sigma) for sigma in sigma_values]

C_mu_drift = [black_scholes_with_drift(S_t, K, T, t, r, mu, sigma) for mu in mu_values]

# Calculate call prices using standard Black-Scholes formula (mu = r)

C_S_standard = [black_scholes_standard(S, K, T, t, r, sigma) for S in S_values]

C_K_standard = [black_scholes_standard(S_t, K, T, t, r, sigma) for K in K_values]

C_T_standard = [black_scholes_standard(S_t, K, T, t, r, sigma) for T in T_values]

C_r_standard = [black_scholes_standard(S_t, K, T, t, r, sigma) for r in r_values]

C_sigma_standard = [black_scholes_standard(S_t, K, T, t, r, sigma) for sigma in sigma_values]

C_mu_standard = [black_scholes_standard(S_t, K, T, t, r, sigma) for mu in mu_values]

# Plotting all dependencies in a single figure for comparison

fig, axs = plt.subplots(3, 2, figsize=(15, 18))

# Current Stock Price (S) comparison

axs[0, 0].plot(S_values, C_S_drift, label="With Drift (mu = 0.1)")

axs[0, 0].plot(S_values, C_S_standard, label="Standard (mu = r)", linestyle="--")

axs[0, 0].set_title('Call Option Price vs Current Stock Price (S)')

axs[0, 0].set_xlabel('Current Stock Price (S)')

axs[0, 0].set_ylabel('Call Option Price (P)')

axs[0, 0].legend()

axs[0, 0].grid(True)

# Strike Price (K) comparison

axs[0, 1].plot(K_values, C_K_drift, label="With Drift (mu = 0.1)")

axs[0, 1].plot(K_values, C_K_standard, label="Standard (mu = r)", linestyle="--")

axs[0, 1].set_title('Call Option Price vs Strike Price (K)')

axs[0, 1].set_xlabel('Strike Price (K)')

axs[0, 1].set_ylabel('Call Option Price (P)')

axs[0, 1].legend()

axs[0, 1].grid(True)

# Time to Maturity (T) comparison

axs[1, 0].plot(T_values, C_T_drift, label="With Drift (mu = 0.1)")

axs[1, 0].plot(T_values, C_T_standard, label="Standard (mu = r)", linestyle="--")

axs[1, 0].set_title('Call Option Price vs Time to Maturity (T)')

axs[1, 0].set_xlabel('Time to Maturity (T)')

axs[1, 0].set_ylabel('Call Option Price (P)')

axs[1, 0].legend()

axs[1, 0].grid(True)

# Risk-Free Interest Rate (r) comparison

axs[1, 1].plot(r_values, C_r_drift, label="With Drift (mu = 0.1)")

axs[1, 1].plot(r_values, C_r_standard, label="Standard (mu = r)", linestyle="--")

axs[1, 1].set_title('Call Option Price vs Risk-Free Interest Rate (r)')

axs[1, 1].set_xlabel('Risk-Free Interest Rate (r)')

axs[1, 1].set_ylabel('Call Option Price (P)')

axs[1, 1].legend()

axs[1, 1].grid(True)

# Volatility (σ) comparison

axs[2, 0].plot(sigma_values, C_sigma_drift, label="With Drift (mu = 0.1)")

axs[2, 0].plot(sigma_values, C_sigma_standard, label="Standard (mu = r)", linestyle="--")

axs[2, 0].set_title('Call Option Price vs Volatility (σ)')

axs[2, 0].set_xlabel('Volatility (σ)')

axs[2, 0].set_ylabel('Call Option Price (P)')

axs[2, 0].legend()

axs[2, 0].grid(True)

# Drift (μ) comparison

axs[2, 1].plot(mu_values, C_mu_drift, label="With Drift (mu = varying)")

axs[2, 1].plot(mu_values, C_mu_standard, label="Standard (mu = r)", linestyle="--")

axs[2, 1].set_title('Call Option Price vs Drift (μ)')

axs[2, 1].set_xlabel('Drift (μ)')

axs[2, 1].set_ylabel('Call Option Price (P)')

axs[2, 1].legend()

axs[2, 1].grid(True)

plt.tight_layout()

plt.show()

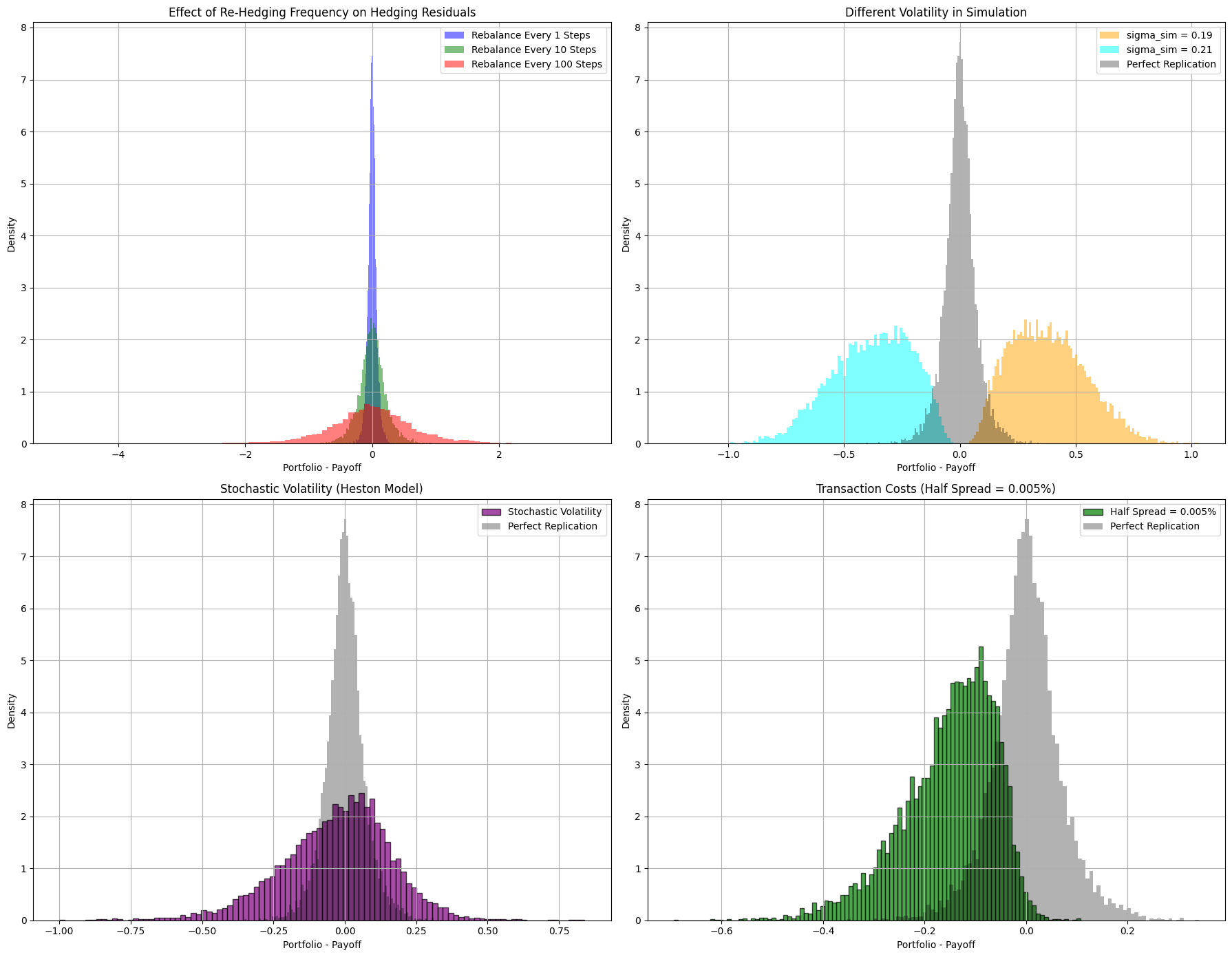

Using the BSM framework in practice#

import numpy as np

import matplotlib.pyplot as plt

from scipy.stats import norm

import pandas as pd

def black_scholes_price(S, K, T, r, sigma, option_type='call'):

"""

Calculate Black-Scholes option price.

"""

d1 = (np.log(S / K) + (r + 0.5 * sigma **2 ) * T ) / (sigma * np.sqrt(T))

d2 = d1 - sigma * np.sqrt(T)

if option_type == 'call':

price = S * norm.cdf(d1) - K * np.exp(-r * T) * norm.cdf(d2)

elif option_type == 'put':

price = K * np.exp(-r * T) * norm.cdf(-d2) - S * norm.cdf(-d1)

else:

raise ValueError("option_type must be 'call' or 'put'")

return price

def black_scholes_delta(S, K, T, r, sigma, option_type='call'):

"""

Calculate Black-Scholes option delta.

"""

d1 = (np.log(S / K) + (r + 0.5 * sigma **2 ) * T ) / (sigma * np.sqrt(T))

if option_type == 'call':

delta = norm.cdf(d1)

elif option_type == 'put':

delta = norm.cdf(d1) - 1

else:

raise ValueError("option_type must be 'call' or 'put'")

return delta

def simulate_gbm_paths(S0, mu, sigma, T, dt, n_paths,

stochastic_vol=False, kappa=2.0, theta=0.04, xi=0.2, rho=-0.7):

"""

Simulate GBM paths with optional stochastic volatility based on the Heston model.

Parameters:

- S0: initial stock price

- mu: drift

- sigma: initial volatility

- T: maturity

- dt: time step

- n_paths: number of simulation paths

- stochastic_vol: if True, use the Heston stochastic volatility model

- kappa: rate of mean reversion of variance (only if stochastic_vol=True)

- theta: long-term variance mean (only if stochastic_vol=True)

- xi: volatility of variance (only if stochastic_vol=True)

- rho: correlation between stock and variance (only if stochastic_vol=True)

Returns:

- paths: array of shape (n_steps +1, n_paths)

"""

n_steps = int(T / dt)

paths = np.zeros((n_steps +1, n_paths))

paths[0] = S0

if stochastic_vol:

# Initialize variance

V0 = sigma ** 2

variances = np.zeros((n_steps +1, n_paths))

variances[0] = V0

# Precompute correlation matrix and Cholesky decomposition

cov_matrix = np.array([[1.0, rho],

[rho, 1.0]])

L = np.linalg.cholesky(cov_matrix)

for t in range(1, n_steps +1):

# Simulate two correlated random variables

Z = np.random.standard_normal((2, n_paths))

correlated_Z = L @ Z

Z_S = correlated_Z[0]

Z_V = correlated_Z[1]

# Update variance using CIR process

V_prev = variances[t-1]

V = V_prev + kappa * (theta - V_prev) * dt + xi * np.sqrt(np.maximum(V_prev, 0)) * np.sqrt(dt) * Z_V

V = np.maximum(V, 0) # Ensure variance is non-negative

variances[t] = V

# Update stock price

S_prev = paths[t-1]

S = S_prev * np.exp( (mu - 0.5 * V_prev) * dt + np.sqrt(V_prev) * np.sqrt(dt) * Z_S )

paths[t] = S

else:

for t in range(1, n_steps +1):

Z = np.random.standard_normal(n_paths)

paths[t] = paths[t-1] * np.exp( (mu - 0.5 * sigma **2 ) * dt + sigma * np.sqrt(dt) * Z )

return paths

def dynamic_hedging(paths, S0, K, T, r, sigma_bs, option_type='call', dt=1/252,

rehedge_freq=1, half_spread=0.0, sigma_sim=None):

"""

Implement dynamic hedging strategy.

Parameters:

- paths: simulated stock price paths (array of shape (n_steps+1, n_paths))

- S0: initial stock price

- K: strike price

- T: maturity

- r: risk-free rate

- sigma_bs: volatility used in BS model

- option_type: 'call' or 'put'

- dt: time step size

- rehedge_freq: frequency of rehedging in terms of number of steps. If 1, rebalance every step.

- half_spread: transaction cost as a fraction of price (half spread for buying and selling)

- sigma_sim: volatility used in simulation (if different from sigma_bs)

Returns:

- differences: array of portfolio - payoff for each path

"""

n_steps, n_paths = paths.shape[0]-1, paths.shape[1]

# Calculate option price and initial delta

option_price = black_scholes_price(S0, K, T, r, sigma_bs, option_type)

option_delta = black_scholes_delta(S0, K, T, r, sigma_bs, option_type)

# Initialize portfolio

portfolio = np.full(n_paths, option_price)

stock_position = np.full(n_paths, option_delta)

cash_position = portfolio - stock_position * S0

# Time steps

times = np.linspace(0, T, n_steps +1)

# Rehedge steps

rehedge_steps = rehedge_freq

for t in range(1, n_steps +1):

tau = T - times[t]

if tau <= 0:

tau = 1e-10 # Avoid division by zero

# Determine if rebalancing is needed

if t % rehedge_steps == 0:

# Compute delta using BS formula

current_S = paths[t]

current_delta = black_scholes_delta(current_S, K, tau, r, sigma_bs, option_type)

# Calculate change in delta

delta_change = current_delta - stock_position

# Calculate transaction cost

transaction_cost = half_spread * np.abs(delta_change * current_S)

# Update cash position

cash_position = cash_position * np.exp(r * dt) - delta_change * current_S - transaction_cost

# Update stock position

stock_position = current_delta

else:

# Just grow the cash position

cash_position = cash_position * np.exp(r * dt)

# Update portfolio value

portfolio = cash_position + stock_position * paths[t]

# Option payoff

if option_type == 'call':

payoff = np.maximum(paths[-1] - K, 0)

elif option_type == 'put':

payoff = np.maximum(K - paths[-1], 0)

else:

raise ValueError("option_type must be 'call' or 'put'")

differences = portfolio - payoff

return differences

def run_simulation():

# Parameters

S0 = 100 # Initial stock price

K = 100 # Strike price

T = 1.0 # 1 year

r = 0.05 # 5% risk-free rate

sigma_bs = 0.20 # 20% volatility used in Black-Scholes model

mu = 0.1 # 10% drift

option_type = 'call'

n_paths = 10000 # Number of simulation paths

dt = 1/10000 # Fixed small time step for accurate approximation

# Perfect setup with varying rehedging frequency

rehedge_freq_values = [1, 10, 100] # Rebalance every 1, 10, 100 steps

differences_rehedge_freq = {}

# Simulate perfect hedging with varying rehedging frequencies

for freq in rehedge_freq_values:

print(f"Simulating Perfect Setup with Rehedging Frequency: Every {freq} steps")

paths_perfect = simulate_gbm_paths(S0, mu, sigma_bs, T, dt, n_paths, stochastic_vol=False)

differences = dynamic_hedging(paths_perfect, S0, K, T, r, sigma_bs, option_type, dt,

rehedge_freq=freq, half_spread=0.0)

differences_rehedge_freq[freq] = differences

# Baseline residuals (Rebalance every step)

residuals_perfect = differences_rehedge_freq[1]

# Violations

# 1. Different volatility for simulation (sigma_sim = 0.19 and 0.21)

sigma_sim_values = [0.19, 0.21]

differences_sigma_sim = {}

for sigma_sim in sigma_sim_values:

print(f"Simulating Different Volatility in Simulation: sigma_sim = {sigma_sim}")

paths_diff_vol = simulate_gbm_paths(S0, mu, sigma_sim, T, dt, n_paths, stochastic_vol=False)

differences = dynamic_hedging(paths_diff_vol, S0, K, T, r, sigma_bs, option_type, dt,

rehedge_freq=1, half_spread=0.0)

differences_sigma_sim[sigma_sim] = differences

# 2. Stochastic Volatility (Heston Model)

print("Simulating Stochastic Volatility (Heston Model)")

paths_stoch_vol = simulate_gbm_paths(S0, mu, sigma_bs, T, dt, n_paths, stochastic_vol=True,

kappa=20.0, theta=0.04, xi=0.2, rho=-0.7)

differences_stoch_vol = dynamic_hedging(paths_stoch_vol, S0, K, T, r, sigma_bs, option_type, dt,

rehedge_freq=1, half_spread=0.0)

# 3. Transaction Costs (Half Spread = 0.005%)

half_spread = 0.00005 # 0.005%

print("Simulating With Transaction Costs (Half Spread = 0.005%)")

paths_half_spread = simulate_gbm_paths(S0, mu, sigma_bs, T, dt, n_paths, stochastic_vol=False)

differences_half_spread = dynamic_hedging(paths_half_spread, S0, K, T, r, sigma_bs, option_type, dt,

rehedge_freq=1, half_spread=half_spread)

# Plot histograms in a 2x2 grid

plt.figure(figsize=(18, 14))

# Subplot 1: Effect of Re-Hedging Frequency on Hedging Residuals

plt.subplot(2, 2, 1)

colors = ['blue', 'green', 'red', 'purple']

labels = [f'Rebalance Every {freq} Steps' for freq in rehedge_freq_values]

for i, freq in enumerate(rehedge_freq_values):

plt.hist(differences_rehedge_freq[freq], bins=100, alpha=0.5,

color=colors[i], label=labels[i], density=True)

plt.title('Effect of Re-Hedging Frequency on Hedging Residuals')

plt.xlabel('Portfolio - Payoff')

plt.ylabel('Density')

plt.legend()

plt.grid(True)

# Subplot 2: Different Volatility in Simulation

plt.subplot(2, 2, 2)

colors_sigma = ['orange', 'cyan']

labels_sigma = [f'sigma_sim = {sigma_sim:.2f}' for sigma_sim in sigma_sim_values]

for i, sigma_sim in enumerate(sigma_sim_values):

plt.hist(differences_sigma_sim[sigma_sim], bins=100, alpha=0.5,

color=colors_sigma[i], label=labels_sigma[i], density=True)

# Add baseline

plt.hist(residuals_perfect, bins=100, alpha=0.3, color='black', label='Perfect Replication', density=True)

plt.title('Different Volatility in Simulation')

plt.xlabel('Portfolio - Payoff')

plt.ylabel('Density')

plt.legend()

plt.grid(True)

# Subplot 3: Stochastic Volatility (Heston Model)

plt.subplot(2, 2, 3)

plt.hist(differences_stoch_vol, bins=100, alpha=0.7, color='purple', edgecolor='black', density=True, label='Stochastic Volatility')

# Add baseline

plt.hist(residuals_perfect, bins=100, alpha=0.3, color='black', label='Perfect Replication', density=True)

plt.title('Stochastic Volatility (Heston Model)')

plt.xlabel('Portfolio - Payoff')

plt.ylabel('Density')

plt.legend()

plt.grid(True)

# Subplot 4: Transaction Costs (Half Spread)

plt.subplot(2, 2, 4)

plt.hist(differences_half_spread, bins=100, alpha=0.7, color='green', edgecolor='black', density=True, label='Half Spread = 0.005%')

# Add baseline

plt.hist(residuals_perfect, bins=100, alpha=0.3, color='black', label='Perfect Replication', density=True)

plt.title('Transaction Costs (Half Spread = 0.005%)')

plt.xlabel('Portfolio - Payoff')

plt.ylabel('Density')

plt.legend()

plt.grid(True)

plt.tight_layout()

plt.show()

# Summary statistics for Perfect Setup with varied rehedging frequency

print("Summary Statistics for Perfect Setup with Varied Re-Hedging Frequency:")

for freq, diff in differences_rehedge_freq.items():

print(f"Rebalance Every {freq} Steps: Mean = {np.mean(diff):.6f}, Std Dev = {np.std(diff):.6f}")

print("-"*60)

# Summary statistics for Violations

print("Summary Statistics for Violations:")

# 1. Different Volatility in Simulation

for sigma_sim, diff in differences_sigma_sim.items():

print(f"Different Volatility in Simulation (sigma_sim = {sigma_sim:.2f}):")

print(f" Mean difference: {np.mean(diff):.6f}")

print(f" Std Dev of difference: {np.std(diff):.6f}")

# 2. Stochastic Volatility (Heston Model)

print("Stochastic Volatility (Heston Model):")

print(f" Mean difference: {np.mean(differences_stoch_vol):.6f}")

print(f" Std Dev of difference: {np.std(differences_stoch_vol):.6f}")

# 3. Transaction Costs (Half Spread)

print("Transaction Costs (Half Spread = 0.005%):")

print(f" Mean difference: {np.mean(differences_half_spread):.6f}")

print(f" Std Dev of difference: {np.std(differences_half_spread):.6f}")

print("-"*40)

if __name__ == "__main__":

run_simulation()

Simulating Perfect Setup with Rehedging Frequency: Every 1 steps

Simulating Perfect Setup with Rehedging Frequency: Every 10 steps

Simulating Perfect Setup with Rehedging Frequency: Every 100 steps

Simulating Different Volatility in Simulation: sigma_sim = 0.19

Simulating Different Volatility in Simulation: sigma_sim = 0.21

Simulating Stochastic Volatility (Heston Model)

Simulating With Transaction Costs (Half Spread = 0.005%)

Summary Statistics for Perfect Setup with Varied Re-Hedging Frequency:

Rebalance Every 1 Steps: Mean = 0.000827, Std Dev = 0.068216

Rebalance Every 10 Steps: Mean = 0.003540, Std Dev = 0.214217

Rebalance Every 100 Steps: Mean = -0.011300, Std Dev = 0.690467

------------------------------------------------------------

Summary Statistics for Violations:

Different Volatility in Simulation (sigma_sim = 0.19):

Mean difference: 0.381420

Std Dev of difference: 0.164161

Different Volatility in Simulation (sigma_sim = 0.21):

Mean difference: -0.381580

Std Dev of difference: 0.172823

Stochastic Volatility (Heston Model):

Mean difference: -0.032125

Std Dev of difference: 0.193527

Transaction Costs (Half Spread = 0.005%):

Mean difference: -0.152493

Std Dev of difference: 0.092860

----------------------------------------