Stochastic Calculus#

Deterministic dynamical systems#

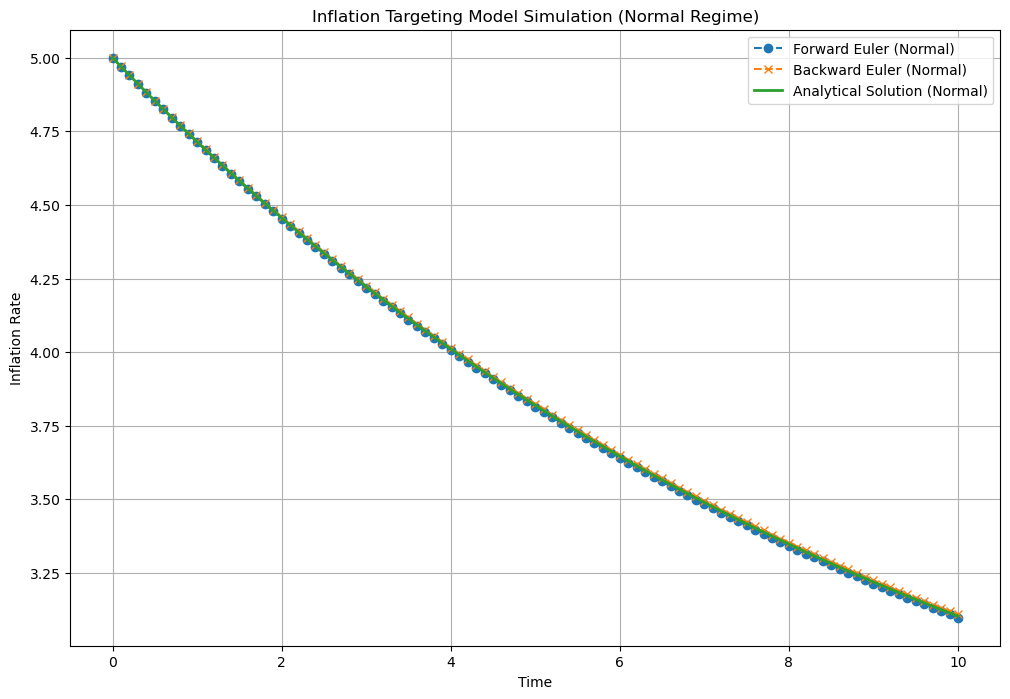

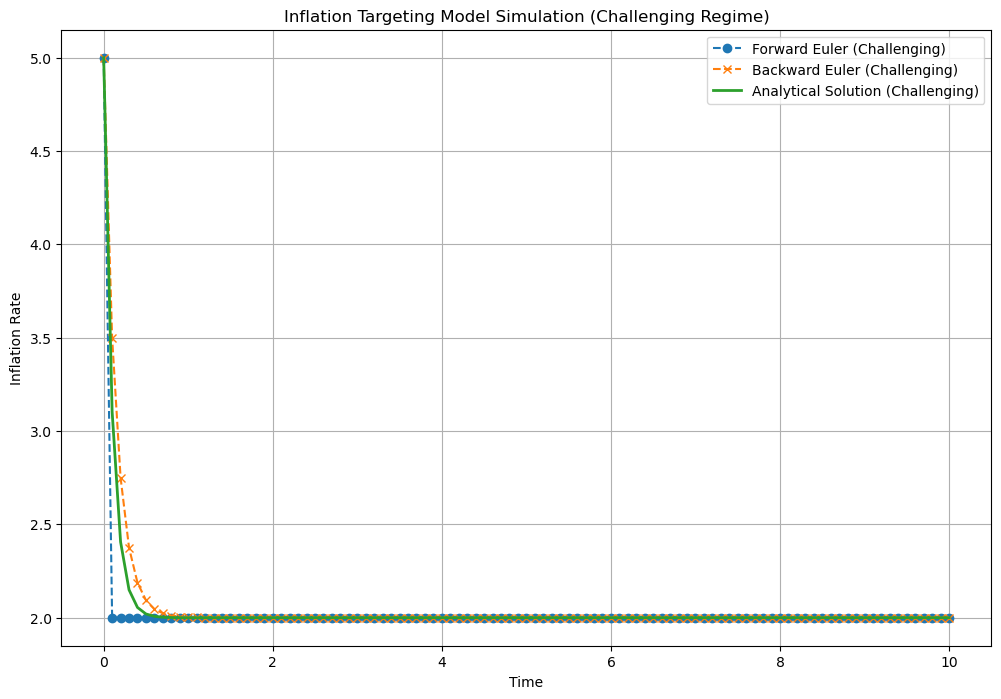

Numerical solution of dynamical systems: inflation targetting#

import numpy as np

import matplotlib.pyplot as plt

def simulate_inflation(theta, pi_hat, pi_t0, Delta, N):

# Time grid

time = np.linspace(0, N * Delta, N + 1)

# Arrays to store the results

pi_forward = np.zeros(N + 1)

pi_backward = np.zeros(N + 1)

pi_analytical = np.zeros(N + 1)

# Initial condition

pi_forward[0] = pi_t0

pi_backward[0] = pi_t0

# Analytical Solution

pi_analytical = pi_hat + (pi_t0 - pi_hat) * np.exp(-theta * time)

# Forward Euler Scheme

for i in range(N):

pi_forward[i + 1] = pi_forward[i] + Delta * theta * (pi_hat - pi_forward[i])

# Backward Euler Scheme

for i in range(N):

pi_backward[i + 1] = (pi_backward[i] + Delta * theta * pi_hat) / (1 + Delta * theta)

return time, pi_forward, pi_backward, pi_analytical

# Parameters for normal regime

theta_normal = 0.1

Delta_normal = 0.1

pi_hat = 2.0

pi_t0 = 5.0

N = 100

# Parameters for challenging regime

theta_challenging = 10.0

Delta_challenging = 0.1

# Simulate for normal regime

time_normal, pi_forward_normal, pi_backward_normal, pi_analytical_normal = simulate_inflation(

theta_normal, pi_hat, pi_t0, Delta_normal, N)

# Simulate for challenging regime

time_challenging, pi_forward_challenging, pi_backward_challenging, pi_analytical_challenging = simulate_inflation(

theta_challenging, pi_hat, pi_t0, Delta_challenging, N)

# Plot the results for normal regime

plt.figure(figsize=(12, 8))

plt.plot(time_normal, pi_forward_normal, label='Forward Euler (Normal)', marker='o', linestyle='--')

plt.plot(time_normal, pi_backward_normal, label='Backward Euler (Normal)', marker='x', linestyle='--')

plt.plot(time_normal, pi_analytical_normal, label='Analytical Solution (Normal)', linestyle='-', linewidth=2)

plt.xlabel('Time')

plt.ylabel('Inflation Rate')

plt.title('Inflation Targeting Model Simulation (Normal Regime)')

plt.legend()

plt.grid(True)

plt.show()

# Plot the results for challenging regime

plt.figure(figsize=(12, 8))

plt.plot(time_challenging, pi_forward_challenging, label='Forward Euler (Challenging)', marker='o', linestyle='--')

plt.plot(time_challenging, pi_backward_challenging, label='Backward Euler (Challenging)', marker='x', linestyle='--')

plt.plot(time_challenging, pi_analytical_challenging, label='Analytical Solution (Challenging)', linestyle='-', linewidth=2)

plt.xlabel('Time')

plt.ylabel('Inflation Rate')

plt.title('Inflation Targeting Model Simulation (Challenging Regime)')

plt.legend()

plt.grid(True)

plt.show()

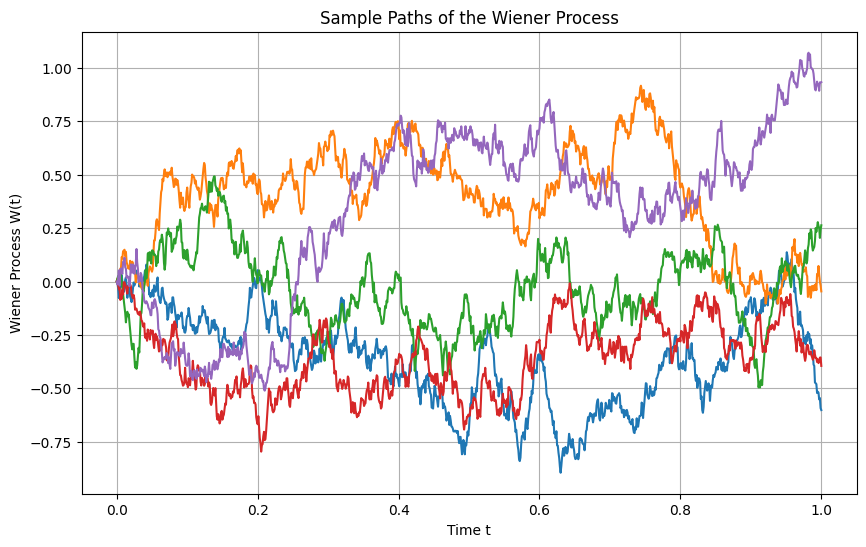

The Wiener Process#

Simulation of the Wiener process (univariate)#

import matplotlib.pyplot as plt

import numpy as np

# Set the parameters for the Wiener process

T = 1.0 # total time

n = 1000 # number of steps

dt = T / n # time increment

t = np.linspace(0, T, n+1) # time points

# Number of paths to simulate

num_paths = 5

# Set up the plot

plt.figure(figsize=(10, 6))

# Simulate multiple paths

for _ in range(num_paths):

W = np.zeros(n+1) # Initialize the Wiener process for each path

for i in range(n):

W[i+1] = W[i] + np.sqrt(dt) * np.random.randn()

plt.plot(t, W, label=f'Path {_+1}')

# Customize the plot

plt.title('Sample Paths of the Wiener Process')

plt.xlabel('Time t')

plt.ylabel('Wiener Process W(t)')

plt.grid(True)

# Show the plot

plt.show()

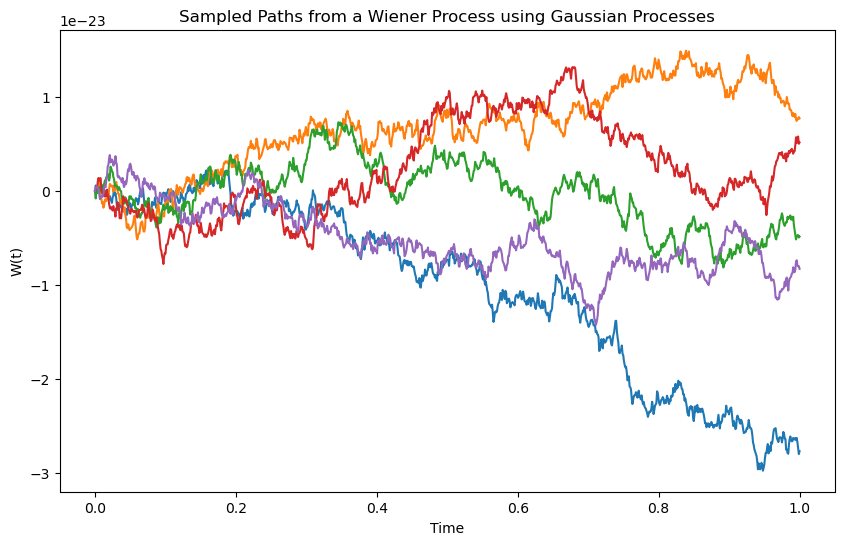

Simulation using Gaussian processes#

import GPy

import numpy as np

import matplotlib.pyplot as plt

# Time points at which to sample the Wiener process

t = np.linspace(0, 1, 1000).reshape(-1, 1)

# Define the Brownian motion kernel

brownian_kernel = GPy.kern.Brownian(input_dim=1, variance=1.0)

# Create a GP model with zero mean function

mean_function = GPy.mappings.Constant(input_dim=1, output_dim=1, value=0)

model = GPy.models.GPRegression(t, np.zeros_like(t), kernel=brownian_kernel, mean_function=mean_function)

# Ensure correct model optimization

model.optimize()

# Sample paths from the GP model

num_samples = 5

samples = model.posterior_samples_f(t, size=num_samples)

# Plot the sampled paths

plt.figure(figsize=(10, 6))

for i in range(num_samples):

plt.plot(t, samples[:, :, i], label=f'Sample {i+1}')

plt.title('Sampled Paths from a Wiener Process using Gaussian Processes')

plt.xlabel('Time')

plt.ylabel('W(t)')

plt.show()

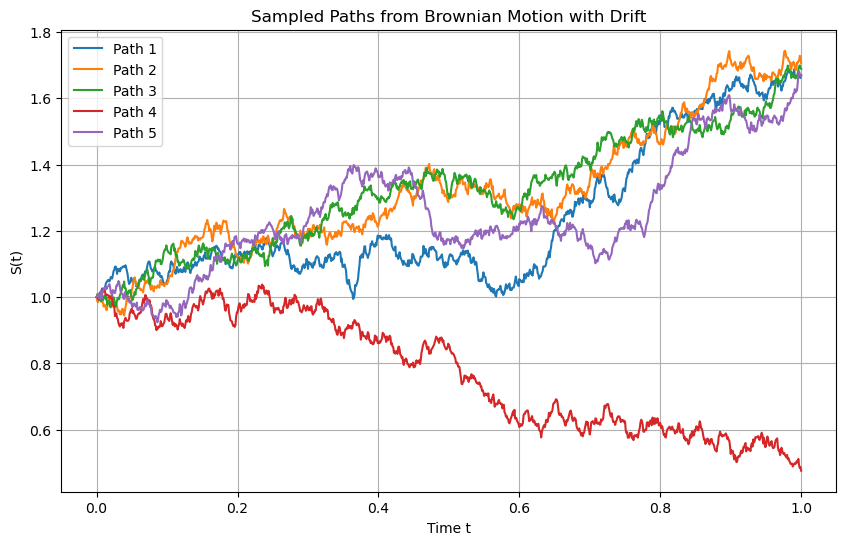

Brownian motion with drift#

Simulation using discrete paths#

import matplotlib.pyplot as plt

import numpy as np

# Set the parameters for Brownian motion with drift and volatility

T = 1.0 # total time

n = 1000 # number of steps

dt = T / n # time increment

t = np.linspace(0, T, n+1) # time points

# Brownian motion parameters

mu = 5 # drift

sigma = 2.0 # volatility

# Number of paths to simulate

num_paths = 5

# Set up the plot

plt.figure(figsize=(10, 6))

# Simulate multiple paths

for _ in range(num_paths):

X = np.zeros(n+1) # Initialize the process for each path

for i in range(n):

X[i+1] = X[i] + mu * dt + sigma * np.sqrt(dt) * np.random.randn()

plt.plot(t, X, label=f'Path {_+1}')

# Customize the plot

plt.title('Sample Paths of Brownian Motion with drift')

plt.xlabel('Time t')

plt.ylabel('X(t)')

plt.grid(True)

# Show the plot

plt.show()

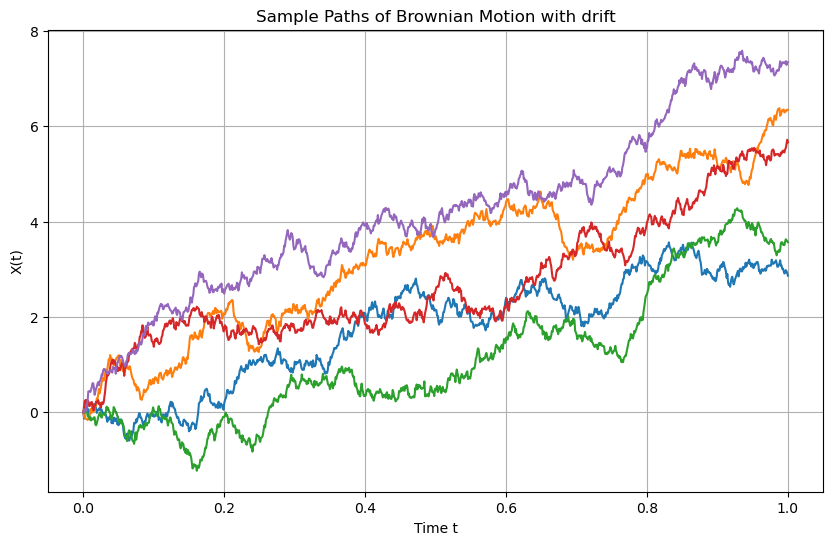

Simulation using Gaussian Processes#

import GPy

import numpy as np

import matplotlib.pyplot as plt

# Parameters for Brownian motion with drift

S0 = 0.0 # Initial value

mu = 0.5 # Drift coefficient

sigma = 0.3 # Volatility

T = 1.0 # Total time

n = 1000 # Number of steps

t = np.linspace(0, T, n+1).reshape(-1, 1) # Time points

# Define the custom kernel for Brownian motion

class BrownianMotionKernel(GPy.kern.Kern):

def __init__(self, input_dim, sigma=1.0, active_dims=None):

super(BrownianMotionKernel, self).__init__(input_dim, active_dims, 'Brownian')

self.sigma = GPy.core.Param('sigma', sigma)

self.link_parameters(self.sigma)

def K(self, X, X2=None):

if X2 is None:

X2 = X

t1 = X

t2 = X2.T

# Covariance function of Brownian motion: sigma^2 * min(s, t)

cov_matrix = self.sigma**2 * np.minimum(t1, t2)

return cov_matrix

def Kdiag(self, X):

return self.sigma**2 * X[:, 0]

# No-op for gradient update since we are not optimizing the kernel

def update_gradients_full(self, dL_dK, X, X2=None):

pass

# No-op for kernel gradient since we are not optimizing the kernel

def gradients_X(self, dL_dK, X, X2=None):

return np.zeros(X.shape)

# Custom mean function to include drift

class BrownianMotionMean(GPy.core.Mapping):

def __init__(self, input_dim, output_dim, S0=0.0, mu=0.0):

super(BrownianMotionMean, self).__init__(input_dim, output_dim)

self.S0 = S0 # Initial value

self.mu = mu # Drift coefficient

def f(self, X):

# Mean function: S0 + mu * t

return self.S0 + self.mu * X

def update_gradients(self, dL_df, X):

pass

def gradients_X(self, dL_df, X):

return np.zeros(X.shape)

# Instantiate the Brownian motion kernel with parameters

bm_kernel = BrownianMotionKernel(input_dim=1, sigma=sigma)

# Instantiate the mean function with S0 and mu

mean_function = BrownianMotionMean(input_dim=1, output_dim=1, S0=S0, mu=mu)

# Provide the initial observation at t=0

t_data = np.array([[0.0]])

Y_data = np.array([[S0]])

# Create a GP model with the custom mean function and Brownian motion kernel

model = GPy.models.GPRegression(t_data, Y_data, kernel=bm_kernel, mean_function=mean_function)

# Set noise variance to a negligible value since we're simulating without observation noise

model.likelihood.variance.fix(1e-10)

# Sample paths from the GP model

num_samples = 5

samples = model.posterior_samples_f(t, size=num_samples)

# Plot the sampled paths

plt.figure(figsize=(10, 6))

for i in range(num_samples):

plt.plot(t, samples[:, :, i], label=f'Path {i+1}')

plt.title(f'Sampled Paths from Brownian Motion with Drift')

plt.xlabel('Time t')

plt.ylabel('S(t)')

plt.grid(True)

plt.legend()

plt.show()

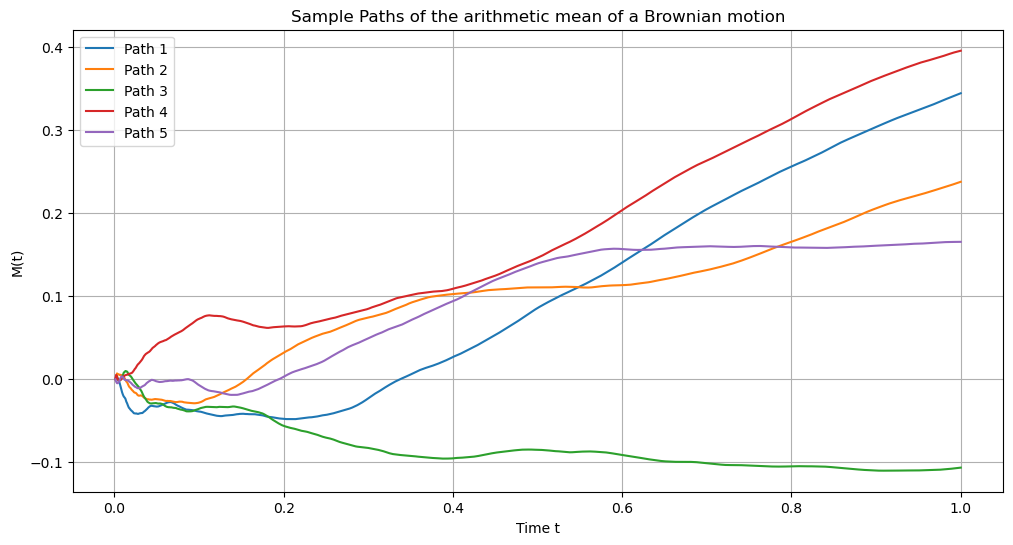

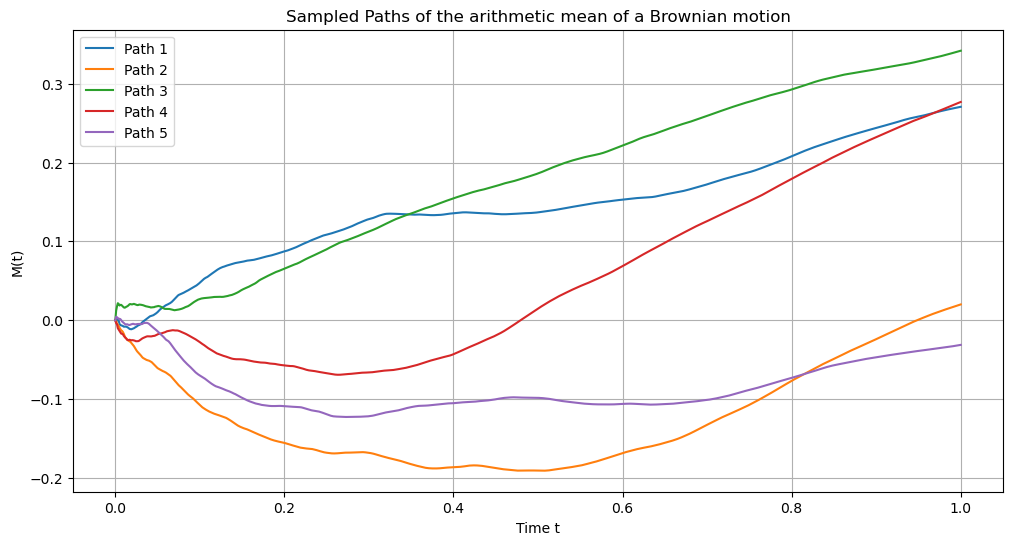

Arithmetic Average of the Brownian Motion#

Simulation using discrete paths#

import matplotlib.pyplot as plt

import numpy as np

# Set the parameters for Brownian motion with drift and volatility

T = 1.0 # total time

n = 1000 # number of steps

dt = T / n # time increment

t = np.linspace(dt, T, n) # time points starting from dt to avoid division by zero

# Brownian motion parameters

S0 = 0.0 # initial value of S_u

mu = 0.5 # drift coefficient

sigma = 0.3 # volatility

# Number of paths to simulate

num_paths = 5

# Initialize array to store M_t for each path

M_t_paths = np.zeros((n, num_paths))

# Set up the plot

plt.figure(figsize=(12, 6))

# Simulate multiple paths

for path in range(num_paths):

# Initialize S_u for each path

S = np.zeros(n + 1) # n+1 because we include S0

S[0] = S0

# Simulate S_u using Euler-Maruyama method

for i in range(n):

dW = np.sqrt(dt) * np.random.randn() # Brownian increment

S[i + 1] = S[i] + mu * dt + sigma * dW

# Compute cumulative sum to approximate the integral

cumulative_S = np.cumsum(S[:-1]) * dt # Exclude the last S[n+1]

# Compute M_t at each time point

M_t = cumulative_S / t

M_t_paths[:, path] = M_t

# Plot the path

plt.plot(t, M_t, label=f'Path {path + 1}')

# Customize the plot

plt.title('Sample Paths of the arithmetic mean of a Brownian motion')

plt.xlabel('Time t')

plt.ylabel('M(t)')

plt.grid(True)

plt.legend()

# Show the plot

plt.show()

Simulation using Gaussian Processes#

import GPy

import numpy as np

import matplotlib.pyplot as plt

# Parameters for Brownian motion with drift

S0 = 0.0 # Initial value

mu = 0.5 # Drift coefficient

sigma = 0.3 # Volatility

T = 1.0 # Total time

n = 1000 # Number of steps

t = np.linspace(1e-6, T, n+1).reshape(-1, 1) # Time points, avoid t=0 to prevent division by zero

# Define the custom kernel based on the provided covariance function

class TimeAverageKernel(GPy.kern.Kern):

def __init__(self, input_dim, sigma=1.0, active_dims=None):

super(TimeAverageKernel, self).__init__(input_dim, active_dims, 'TimeAverage')

self.sigma = GPy.core.Param('sigma', sigma)

self.link_parameters(self.sigma)

def K(self, X, X2=None):

if X2 is None:

X2 = X

t1 = X[:, 0].reshape(-1, 1) # Column vector

t2 = X2[:, 0].reshape(1, -1) # Row vector

t_min = np.minimum(t1, t2)

t_max = np.maximum(t1, t2)

# Compute the covariance matrix using the given formula

cov_matrix = self.sigma ** 2 * (t_min / 2) * (1 - t_min / (3 * t_max))

return cov_matrix

def Kdiag(self, X):

t = X[:, 0]

# Compute the diagonal elements of the covariance matrix

cov_diag = self.sigma ** 2 * (t / 2) * (1 - t / (3 * t))

# Simplify the expression

cov_diag = self.sigma ** 2 * (t / 2) * (1 - 1 / 3)

cov_diag = self.sigma ** 2 * (t / 2) * (2 / 3)

cov_diag = self.sigma ** 2 * t * (1 / 3)

return cov_diag

def update_gradients_full(self, dL_dK, X, X2=None):

pass

def gradients_X(self, dL_dK, X, X2=None):

return np.zeros(X.shape)

# Custom mean function to include drift

class TimeAverageMean(GPy.core.Mapping):

def __init__(self, input_dim, output_dim, S0=0.0, mu=0.0):

super(TimeAverageMean, self).__init__(input_dim, output_dim)

self.S0 = S0 # Initial value

self.mu = mu # Drift coefficient

def f(self, X):

t = X[:, 0]

mean = self.S0 + 0.5 * self.mu * t

return mean.reshape(-1, 1)

def update_gradients(self, dL_df, X):

pass

def gradients_X(self, dL_df, X):

return np.zeros(X.shape)

# Instantiate the Time Average kernel with parameters

ta_kernel = TimeAverageKernel(input_dim=1, sigma=sigma)

# Instantiate the mean function with S0 and mu

mean_function = TimeAverageMean(input_dim=1, output_dim=1, S0=S0, mu=mu)

# Provide the initial observation at t=1e-6 (approaching zero)

t_data = np.array([[1e-6]])

Y_data = mean_function.f(t_data) # Mean at t=1e-6

# Create a GP model with the custom mean function and Time Average kernel

model = GPy.models.GPRegression(t_data, Y_data, kernel=ta_kernel, mean_function=mean_function)

# Set noise variance to a negligible value since we're simulating without observation noise

model.likelihood.variance.fix(1e-10)

# Sample paths from the GP model

num_samples = 5

samples = model.posterior_samples_f(t, size=num_samples)

# Plot the sampled paths

plt.figure(figsize=(12, 6))

for i in range(num_samples):

plt.plot(t, samples[:, :, i], label=f'Path {i+1}')

plt.title('Sampled Paths of the arithmetic mean of a Brownian motion')

plt.xlabel('Time t')

plt.ylabel('M(t)')

plt.grid(True)

plt.legend()

plt.show()

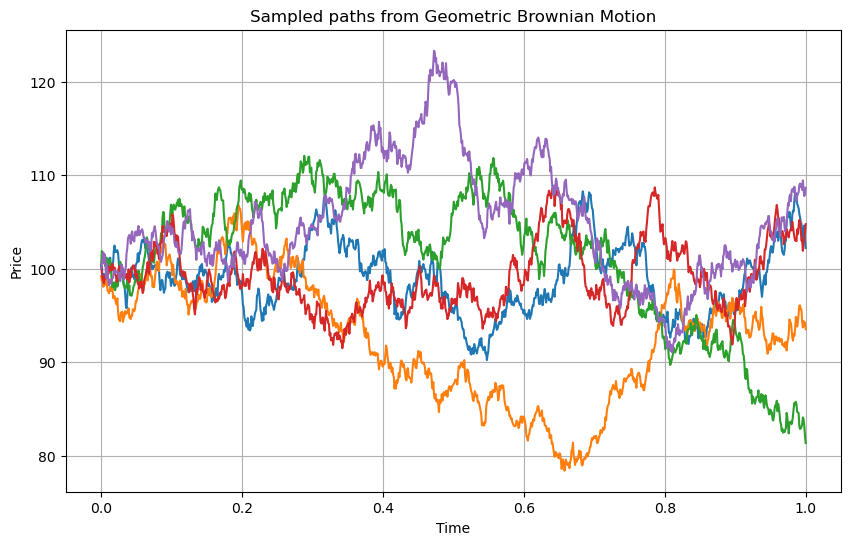

Geometric Brownian Motion#

Simulation using discrete paths#

import numpy as np

import matplotlib.pyplot as plt

def simulate_gbm(S0, mu, sigma, T, N, num_paths):

dt = T / N

t = np.linspace(0, T, N)

paths = []

for _ in range(num_paths):

W = np.random.normal(0, np.sqrt(dt), N)

W = np.cumsum(W) # cumulative sum to represent Brownian motion

S = S0 * np.exp((mu - 0.5 * sigma**2) * t + sigma * W)

paths.append(S)

return t, paths

# Parameters

S0 = 100 # Initial value of the asset

mu = 0.05 # Drift

sigma = 0.2 # Volatility

T = 1 # Time horizon (1 year)

N = 1000 # Number of time steps

num_paths = 5 # Number of paths to simulate

t, paths = simulate_gbm(S0, mu, sigma, T, N, num_paths)

# Plotting the simulated GBM paths

plt.figure(figsize=(10, 6))

for i, S in enumerate(paths):

plt.plot(t, S, label=f'Path {i + 1}')

plt.xlabel('Time')

plt.ylabel('Price')

plt.title('Sampled paths from Geometric Brownian Motion')

plt.grid(True)

plt.show()

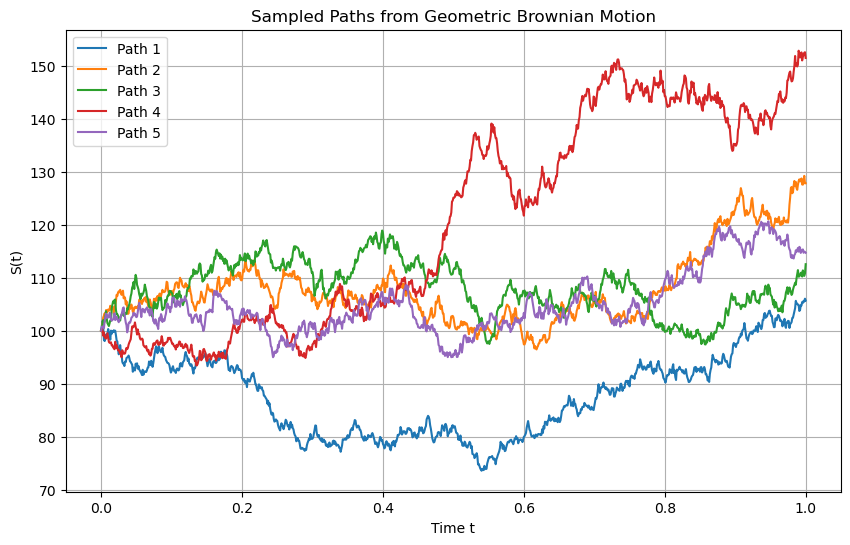

Simulation using Gaussian Processes#

import GPy

import numpy as np

import matplotlib.pyplot as plt

# Parameters for Geometric Brownian Motion

S0 = 100 # Initial value of the asset

mu = 0.05 # Drift

sigma = 0.2 # Volatility

T = 1 # Time horizon (1 year)

n = 1000 # Number of steps

t = np.linspace(0, T, n+1).reshape(-1, 1) # Time points

# Define the custom kernel for Brownian motion

class GBMKernel(GPy.kern.Kern):

def __init__(self, input_dim, sigma=1.0, active_dims=None):

super(GBMKernel, self).__init__(input_dim, active_dims, 'Brownian')

self.sigma = GPy.core.Param('sigma', sigma)

self.link_parameters(self.sigma)

def K(self, X, X2=None):

if X2 is None:

X2 = X

t1 = X

t2 = X2.T

# Covariance function of Brownian motion: sigma^2 * min(s, t)

cov_matrix = self.sigma**2 * np.minimum(t1, t2)

return cov_matrix

def Kdiag(self, X):

return self.sigma**2 * X[:, 0]

# No-op for gradient update since we are not optimizing the kernel

def update_gradients_full(self, dL_dK, X, X2=None):

pass

# No-op for kernel gradient since we are not optimizing the kernel

def gradients_X(self, dL_dK, X, X2=None):

return np.zeros(X.shape)

# Custom mean function to include drift

class GBMMean(GPy.core.Mapping):

def __init__(self, input_dim, output_dim, S0=0.0, mu=0.0):

super(GBMMean, self).__init__(input_dim, output_dim)

self.S0 = S0 # Initial value

self.mu = mu # Drift coefficient

def f(self, X):

# Mean function: S0 + mu * t

return self.S0 + self.mu * X

def update_gradients(self, dL_df, X):

pass

def gradients_X(self, dL_df, X):

return np.zeros(X.shape)

# Instantiate the Brownian motion kernel with parameters

bm_kernel = GBMKernel(input_dim=1, sigma=sigma)

# Instantiate the mean function with S0 and mu

mean_function = GBMMean(input_dim=1, output_dim=1, S0=np.log(S0), mu=mu)

# Provide the initial observation at t=0

t_data = np.array([[0.0]])

Y_data = np.array([[np.log(S0)]])

# Create a GP model with the custom mean function and Brownian motion kernel

model = GPy.models.GPRegression(t_data, Y_data, kernel=bm_kernel, mean_function=mean_function)

# Set noise variance to a negligible value since we're simulating without observation noise

model.likelihood.variance.fix(1e-10)

# Sample paths from the GP model

num_samples = 5

samples = model.posterior_samples_f(t, size=num_samples)

# Transform samples to original GBM scale

gbm_samples = np.exp(samples)

# Plot the sampled paths

plt.figure(figsize=(10, 6))

for i in range(num_samples):

plt.plot(t, gbm_samples[:, :, i], label=f'Path {i+1}')

plt.title(f'Sampled Paths from Geometric Brownian Motion')

plt.xlabel('Time t')

plt.ylabel('S(t)')

plt.grid(True)

plt.legend()

plt.show()

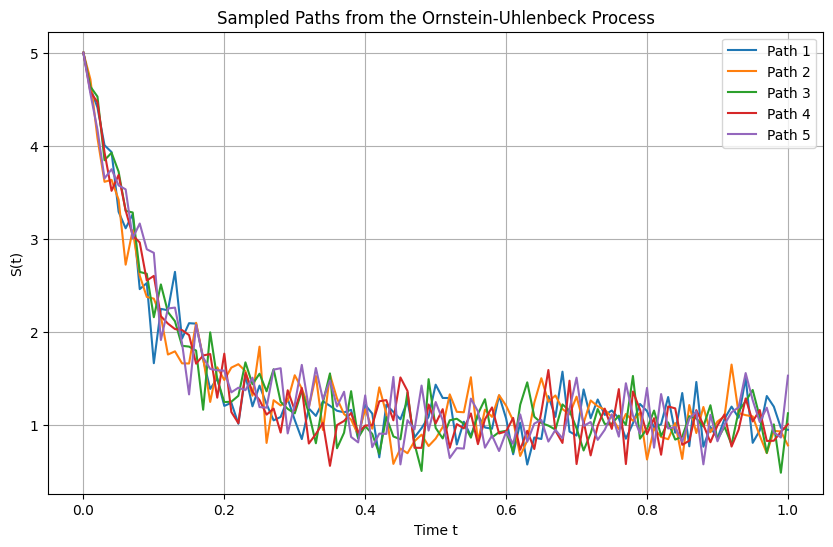

Orstein - Uhlenbeck process#

Simulation using discrete paths#

import numpy as np

import matplotlib.pyplot as plt

# Parameters for the Ornstein-Uhlenbeck process

S0 = 5.0 # Initial value

mu = 1.0 # Long-term mean

theta = 10 # Rate of mean reversion

sigma = 1 # Volatility

T = 1.0 # Total time

n = 100 # Number of steps

dt = T / n # Time step size

t = np.linspace(0, T, n+1) # Time points

# Number of paths to simulate

num_paths = 5

# Set up the plot

plt.figure(figsize=(10, 6))

# Simulate multiple paths

for _ in range(num_paths):

S = np.zeros(n+1) # Initialize the process

S[0] = S0 # Set initial value

for i in range(1, n+1):

# Compute the mean and variance for the next step

mean = S0 * np.exp(-theta * t[i]) + mu * (1 - np.exp(-theta * t[i]))

variance = (sigma**2 / (2 * theta)) * (1 - np.exp(-2 * theta * t[i]))

# Sample from the normal distribution with the computed mean and variance

S[i] = np.random.normal(mean, np.sqrt(variance))

# Plot the Ornstein-Uhlenbeck path

plt.plot(t, S, label=f'Path {_+1}')

# Customize the plot

plt.title('Sampled Paths from the Ornstein-Uhlenbeck Process')

plt.xlabel('Time t')

plt.ylabel('S(t)')

plt.grid(True)

plt.legend()

plt.show()

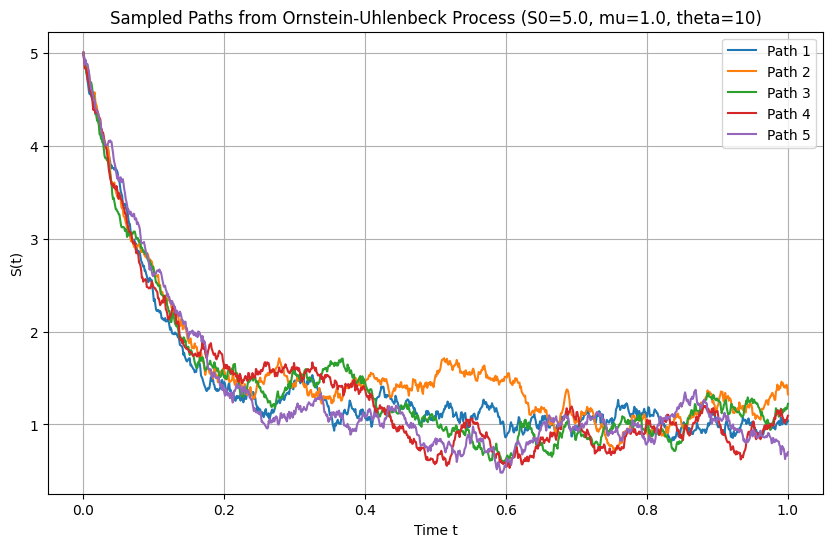

Simulation using Gaussian Processes#

import GPy

import numpy as np

import matplotlib.pyplot as plt

# Parameters for the Ornstein-Uhlenbeck process

S0 = 5.0 # Initial value

mu = 1.0 # Long-term mean

theta = 10 # Rate of mean reversion

sigma = 1 # Volatility

T = 1.0 # Total time

n = 1000 # Number of steps

t = np.linspace(0, T, n+1).reshape(-1, 1) # Time points

# Define the custom kernel for the Ornstein-Uhlenbeck process

class OrnsteinUhlenbeckKernel(GPy.kern.Kern):

def __init__(self, input_dim, theta=1.0, sigma=1.0, active_dims=None):

super(OrnsteinUhlenbeckKernel, self).__init__(input_dim, active_dims, 'OU')

self.theta = GPy.core.Param('theta', theta)

self.sigma = GPy.core.Param('sigma', sigma)

self.link_parameters(self.theta, self.sigma)

def K(self, X, X2=None):

if X2 is None:

X2 = X

t1 = X

t2 = X2.T

min_t = np.minimum(t1, t2)

# Covariance function of the Ornstein-Uhlenbeck process

cov_matrix = (self.sigma**2 / (2 * self.theta)) * np.exp(-self.theta * np.abs(t1 - t2)) * (1 - np.exp(-2 * self.theta * min_t))

return cov_matrix

def Kdiag(self, X):

return (self.sigma**2 / (2 * self.theta)) * (1 - np.exp(-2 * self.theta * X[:, 0]))

# No-op for gradient update since we are not optimizing the kernel

def update_gradients_full(self, dL_dK, X, X2=None):

pass

# No-op for kernel gradient since we are not optimizing the kernel

def gradients_X(self, dL_dK, X, X2=None):

return np.zeros(X.shape)

# Custom mean function to include mean-reverting drift toward mu

class OUProcessMean(GPy.core.Mapping):

def __init__(self, input_dim, output_dim, S0=0.0, mu=0.0, theta=1.0):

super(OUProcessMean, self).__init__(input_dim, output_dim)

self.S0 = S0 # Initial value

self.mu = mu # Long-term mean

self.theta = theta # Rate of mean reversion

def f(self, X):

# Mean function: S_0 * exp(-theta * t) + mu * (1 - exp(-theta * t))

return self.S0 * np.exp(-self.theta * X) + self.mu * (1 - np.exp(-self.theta * X))

def update_gradients(self, dL_df, X):

pass

def gradients_X(self, dL_df, X):

return np.zeros(X.shape)

# Instantiate the OU kernel with parameters

ou_kernel = OrnsteinUhlenbeckKernel(input_dim=1, theta=theta, sigma=sigma)

# Instantiate the mean function with non-zero initial value S0 and long-term mean mu

mean_function = OUProcessMean(input_dim=1, output_dim=1, S0=S0, mu=mu, theta=theta)

# Provide the initial observation at t=0

t_data = np.array([[0.0]])

Y_data = np.array([[S0]])

# Create a GP model with the custom mean function and OU kernel

model = GPy.models.GPRegression(t_data, Y_data, kernel=ou_kernel, mean_function=mean_function)

# Set noise variance to a negligible value since we're simulating without observation noise

model.likelihood.variance.fix(1e-10)

# Sample paths from the GP model

num_samples = 5

samples = model.posterior_samples_f(t, size=num_samples)

# Plot the sampled paths

plt.figure(figsize=(10, 6))

for i in range(num_samples):

plt.plot(t, samples[:, :, i], label=f'Path {i+1}')

plt.title(f'Sampled Paths from Ornstein-Uhlenbeck Process (S0={S0}, mu={mu}, theta={theta})')

plt.xlabel('Time t')

plt.ylabel('S(t)')

plt.grid(True)

plt.legend()

plt.show()

Brownian bridge#

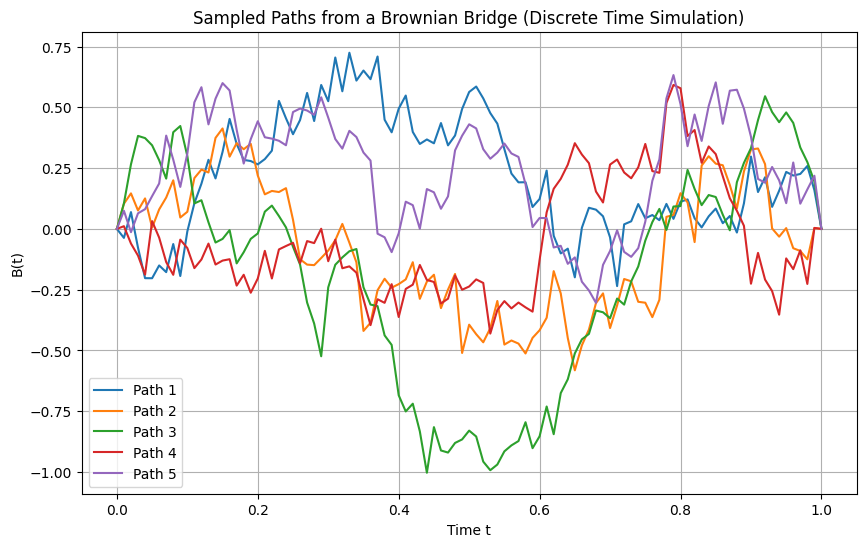

Simulation using discrete paths#

import numpy as np

import matplotlib.pyplot as plt

# Parameters for the Brownian bridge

T = 1.0 # Total time

n = 100 # Number of steps

dt = T / n # Time step size

t = np.linspace(0, T, n+1) # Time points

# Number of paths to simulate

num_paths = 5

# Set up the plot

plt.figure(figsize=(10, 6))

# Simulate multiple paths

for _ in range(num_paths):

W = np.zeros(n+1) # Initialize the Wiener process

for i in range(1, n+1):

W[i] = W[i-1] + np.sqrt(dt) * np.random.randn() # Standard Wiener process

# Adjust Wiener process to form a Brownian bridge

B = W - (t / T) * W[-1] # Brownian bridge: W(t) - (t/T) * W(T)

# Plot the Brownian bridge path

plt.plot(t, B, label=f'Path {_+1}')

# Customize the plot

plt.title('Sampled Paths from a Brownian Bridge (Discrete Time Simulation)')

plt.xlabel('Time t')

plt.ylabel('B(t)')

plt.grid(True)

plt.legend()

plt.show()

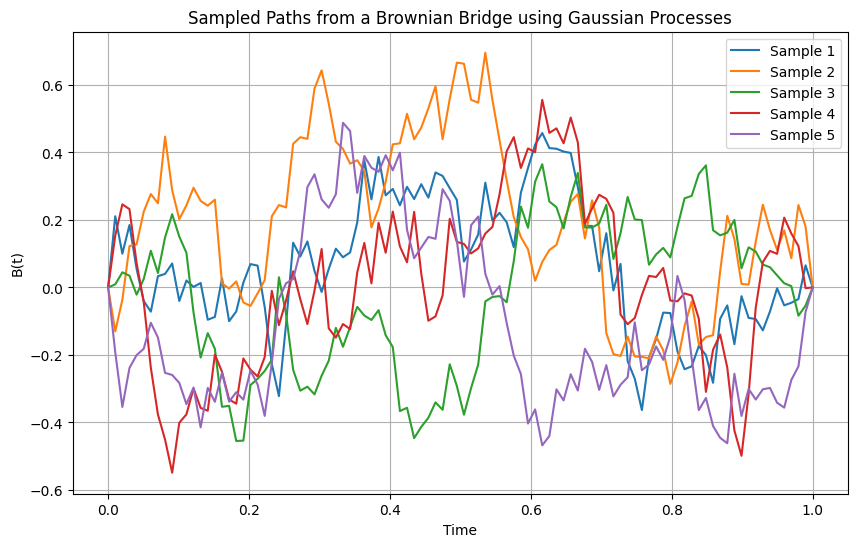

Simulation using Gaussian processes#

import GPy

import numpy as np

import matplotlib.pyplot as plt

# Time points at which to sample the Brownian bridge

T = 1.0

t = np.linspace(0, T, 100).reshape(-1, 1)

# Define a custom kernel for the Brownian bridge

class BrownianBridgeKernel(GPy.kern.Kern):

def __init__(self, input_dim, variance=1.0, active_dims=None):

super(BrownianBridgeKernel, self).__init__(input_dim, active_dims, 'brownian_bridge')

self.variance = GPy.core.Param('variance', variance)

self.link_parameter(self.variance)

def K(self, X, X2=None):

if X2 is None:

X2 = X

t1 = X

t2 = X2.T

T = np.max(X)

# Brownian bridge kernel: min(t1, t2) - (t1 * t2) / T

cov_matrix = np.minimum(t1, t2) - (t1 * t2) / T

return self.variance * cov_matrix

def Kdiag(self, X):

return self.variance * (X[:, 0] - (X[:, 0]**2) / T)

# No-op for gradient update since we are not optimizing the kernel

def update_gradients_full(self, dL_dK, X, X2=None):

pass

# No-op for kernel gradient since we are not optimizing the kernel

def gradients_X(self, dL_dK, X, X2=None):

return np.zeros(X.shape)

# Instantiate the Brownian bridge kernel with variance 1

brownian_bridge_kernel = BrownianBridgeKernel(input_dim=1, variance=1.0)

# Create a GP model with zero mean function

mean_function = GPy.mappings.Constant(input_dim=1, output_dim=1, value=0)

model = GPy.models.GPRegression(t, np.zeros_like(t), kernel=brownian_bridge_kernel, mean_function=mean_function)

# Sample paths from the GP model without optimizing (since Brownian bridge doesn't require fitting)

num_samples = 5

samples = model.posterior_samples_f(t, size=num_samples)

# Plot the sampled paths

plt.figure(figsize=(10, 6))

for i in range(num_samples):

plt.plot(t, samples[:, :, i], label=f'Sample {i+1}')

plt.title('Sampled Paths from a Brownian Bridge using Gaussian Processes')

plt.xlabel('Time')

plt.ylabel('B(t)')

plt.grid(True)

plt.legend()

plt.show()

Jump processes#

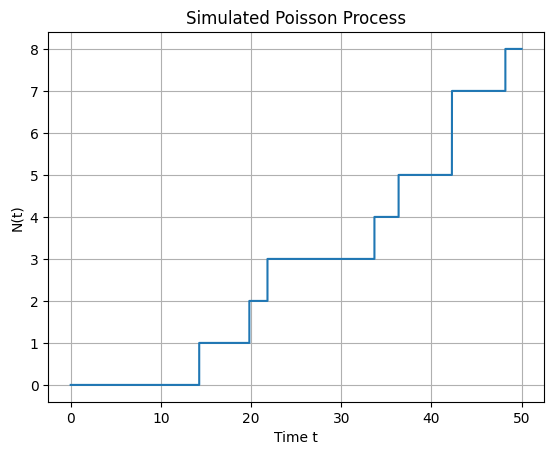

Homogeneous Poisson process simulation#

import numpy as np

import matplotlib.pyplot as plt

# Parameters

lambda_rate = 0.2 # The rate parameter λ of the Poisson process

T = 50 # Total time

delta_t = 0.01 # Time-step Δt

num_steps = int(T / delta_t) # Number of time steps

# Time grid

t = np.linspace(0, T, num_steps + 1)

# Initialize N_t

N_t = np.zeros(num_steps + 1, dtype=int)

# Simulate the Poisson process

for i in range(1, num_steps + 1):

# Generate a random number between 0 and 1

u = np.random.rand()

# If u < λΔt, increment N_t

if u < lambda_rate * delta_t:

N_t[i] = N_t[i - 1] + 1

else:

N_t[i] = N_t[i - 1]

# Plot the Poisson process

plt.step(t, N_t, where='post')

plt.xlabel('Time t')

plt.ylabel('N(t)')

plt.title('Simulated Poisson Process')

plt.grid(True)

plt.show()

Hawkes process#

import numpy as np

import matplotlib.pyplot as plt

# Parameters

mu = 0.2 # Baseline intensity (μ)

alpha = 0.5 # Excitation parameter (α)

beta = 1 # Decay rate (β)

T = 50 # Total time to simulate

delta_t = 0.01 # Time-step Δt

# Time grid

time_grid = np.arange(0, T + delta_t, delta_t)

num_steps = len(time_grid)

# Initialize N_t and event times

N_t = np.zeros(num_steps, dtype=int)

event_times = []

# Simulate the Hawkes process

for i in range(1, num_steps):

t_i = time_grid[i]

# Compute lambda_t

lambda_t = mu

if event_times:

tau_array = np.array(event_times)

lambda_t += np.sum(alpha * np.exp(-beta * (t_i - tau_array)))

# Calculate the event probability

p = lambda_t * delta_t

if p > 1.0:

p = 1.0 # Ensure probability does not exceed 1

# Simulate event occurrence

u = np.random.rand()

if u < p:

N_t[i] = N_t[i - 1] + 1

event_times.append(t_i)

else:

N_t[i] = N_t[i - 1]

# Plot the counting process

#plt.figure(figsize=(12, 6))

plt.step(time_grid, N_t, where='post')

plt.xlabel('Time t')

plt.ylabel('N(t)')

plt.title('Simulated Hawkes Process')

plt.grid(True)

plt.show()

Compound Poisson process#

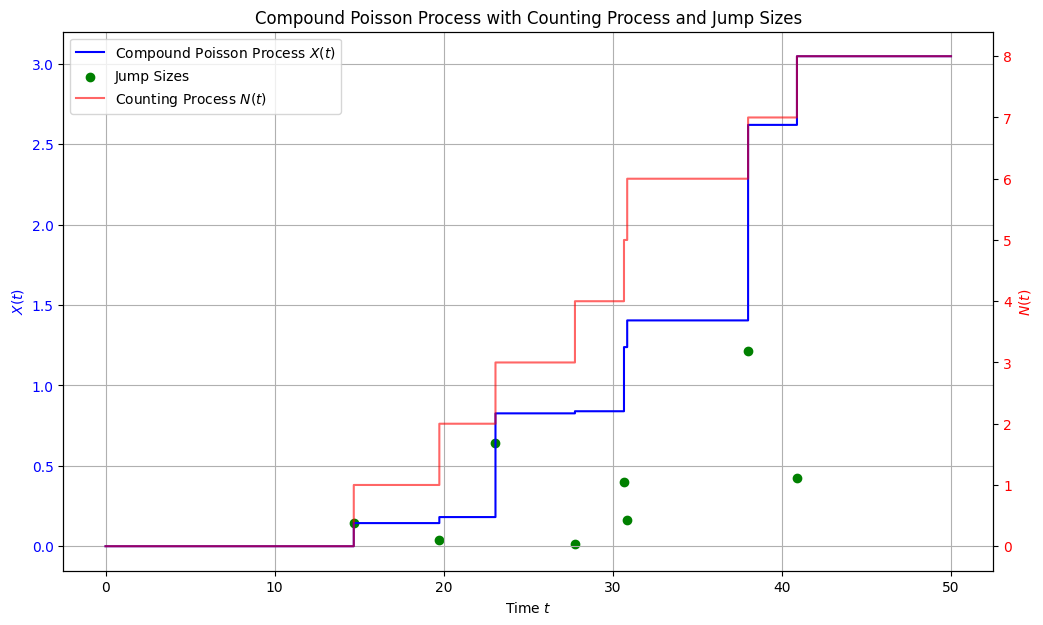

import numpy as np

import matplotlib.pyplot as plt

# Parameters

lambda_rate = 0.2 # Rate parameter λ of the Poisson process

T = 50 # Total simulation time

delta_t = 0.01 # Time-step Δt

num_steps = int(T / delta_t)

time_grid = np.linspace(0, T, num_steps + 1)

# Jump size distribution parameters

eta = 2.5 # Rate parameter of the exponential distribution for jump sizes

# Initialize arrays

N_t = np.zeros(num_steps + 1, dtype=int) # Counting process N(t)

X_t = np.zeros(num_steps + 1) # Compound Poisson process X(t)

event_times = [] # Times when events occur

jump_sizes = [] # Sizes of the jumps

# Simulate the compound Poisson process

for i in range(1, num_steps + 1):

t = time_grid[i]

# Probability of an event in [t_i, t_i + delta_t)

p = lambda_rate * delta_t

# Ensure probability does not exceed 1

p = min(p, 1.0)

# Determine if an event occurs

if np.random.rand() < p:

N_t[i] = N_t[i - 1] + 1

# Sample a jump size Y_i from an exponential distribution

Y_i = np.random.exponential(scale=1/eta)

jump_sizes.append(Y_i)

event_times.append(t)

X_t[i] = X_t[i - 1] + Y_i

else:

N_t[i] = N_t[i - 1]

X_t[i] = X_t[i - 1]

# Plot all three visualizations in one figure

fig, ax1 = plt.subplots(figsize=(12, 7))

# Plot the compound Poisson process X(t)

ax1.step(time_grid, X_t, where='post', label='Compound Poisson Process $X(t)$', color='blue')

ax1.set_xlabel('Time $t$')

ax1.set_ylabel('$X(t)$', color='blue')

ax1.tick_params(axis='y', labelcolor='blue')

ax1.grid(True)

# Plot jump sizes as scatter points on X(t)

event_indices = [np.searchsorted(time_grid, t) for t in event_times]

event_values = [X_t[idx] for idx in event_indices]

ax1.scatter(event_times, jump_sizes, color='green', marker='o', label='Jump Sizes')

# Create a secondary y-axis for the counting process N(t)

ax2 = ax1.twinx()

ax2.step(time_grid, N_t, where='post', label='Counting Process $N(t)$', color='red', alpha=0.6)

ax2.set_ylabel('$N(t)$', color='red')

ax2.tick_params(axis='y', labelcolor='red')

# Combine legends from both axes

lines1, labels1 = ax1.get_legend_handles_labels()

lines2, labels2 = ax2.get_legend_handles_labels()

ax1.legend(lines1 + lines2, labels1 + labels2, loc='upper left')

plt.title('Compound Poisson Process with Counting Process and Jump Sizes')

plt.show()

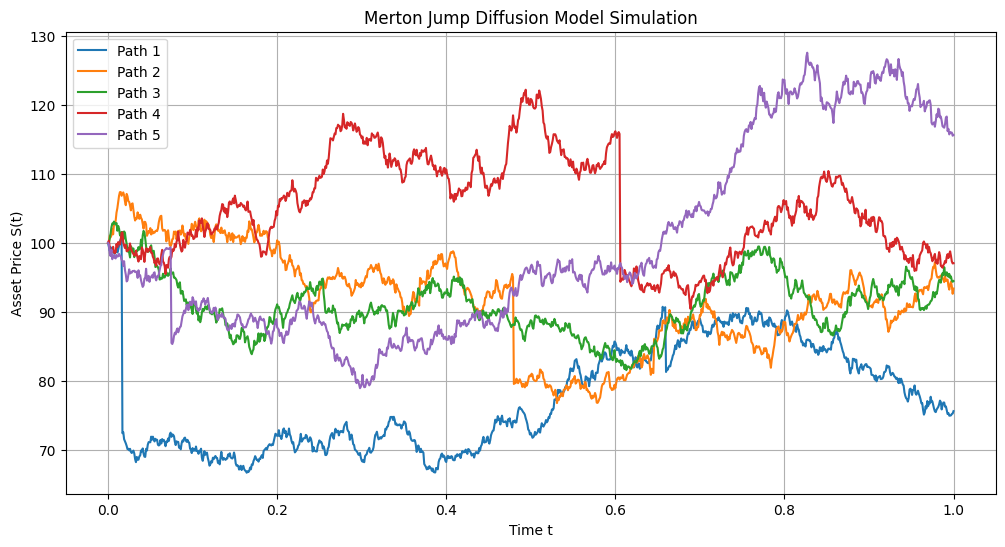

Jump diffusion processes#

import numpy as np

import matplotlib.pyplot as plt

def simulate_merton_jump_diffusion(S0, mu, sigma, lamb, mu_j, sigma_j, T, N, M):

"""

Simulate the Merton jump diffusion model.

Parameters:

- S0: Initial asset price.

- mu: Expected return (drift rate).

- sigma: Volatility of the continuous component.

- lamb: Jump intensity (average number of jumps per unit time).

- mu_j: Mean of the jump size distribution (of ln(J)).

- sigma_j: Standard deviation of the jump size distribution (of ln(J)).

- T: Total time horizon.

- N: Number of time steps.

- M: Number of simulation paths.

Returns:

- t: Array of time points.

- S: Matrix of simulated asset prices (M paths x N+1 time points).

"""

dt = T / N # Time step size

t = np.linspace(0, T, N + 1) # Time grid

# Precompute constants

drift = (mu - 0.5 * sigma**2) * dt

diffusion = sigma * np.sqrt(dt)

# Initialize asset price paths

S = np.zeros((M, N + 1))

S[:, 0] = S0

for m in range(M):

# Initialize variables for each path

S_m = np.zeros(N + 1)

S_m[0] = S0

# Generate random numbers for Brownian motion

Z = np.random.normal(size=N)

# Generate random numbers for jumps

# Poisson random numbers for number of jumps in each time step

Nt = np.random.poisson(lamb * dt, size=N)

# Total number of jumps

num_jumps = np.sum(Nt)

# Generate jump sizes only where jumps occur

if num_jumps > 0:

jump_sizes = np.random.normal(loc=mu_j, scale=sigma_j, size=num_jumps)

else:

jump_sizes = np.array([])

# Index to keep track of jump sizes

jump_index = 0

for i in range(1, N + 1):

# Continuous part

S_m[i] = S_m[i - 1] * np.exp(drift + diffusion * Z[i - 1])

# Jump part

if Nt[i - 1] > 0:

# Apply jumps

total_jump = np.sum(jump_sizes[jump_index:jump_index + Nt[i - 1]])

S_m[i] *= np.exp(total_jump)

jump_index += Nt[i - 1]

S[m, :] = S_m

return t, S

# Parameters

S0 = 100 # Initial asset price

mu = 0.1 # Expected return

sigma = 0.2 # Volatility

lamb = 1 # Jump intensity λ

k = -0.1 # Mean of ln(J) (jump sizes)

delta = 0.1 # Std dev of ln(J)

T = 1.0 # Total time (e.g., 1 year)

N = 1000 # Number of time steps

M = 5 # Number of simulation paths

# Simulate the Merton jump diffusion model

t, S = simulate_merton_jump_diffusion(S0, mu, sigma, lamb, k, delta, T, N, M)

# Plot the simulated asset price paths

plt.figure(figsize=(12, 6))

for m in range(M):

plt.plot(t, S[m, :], label=f'Path {m + 1}')

plt.xlabel('Time t')

plt.ylabel('Asset Price S(t)')

plt.title('Merton Jump Diffusion Model Simulation')

plt.legend()

plt.grid(True)

plt.show()